Thailand's Economic Outlook: Q2 and Beyond

In Q2, Thailand's economy showed slow growth, with income concentrated in tourism-related services. The agricultural sector is gradually recovering, but manufacturing is contracting, raising concerns. Households are cautious about spending, and private investment, particularly in construction, is slowing. Exports have yet to show clear recovery. However, from May onwards, government spending and investment have begun to expand, potentially preventing economic decline.

For the latter half of 2024, Thailand's economy is expected to grow more robustly, supported by tourism, private consumption, investment, and exports. Domestic demand will gradually recover. Political uncertainties may temporarily reduce investor and consumer confidence, but the main risks include geopolitical tensions, elections in various countries that might shift political power, persistently high-interest rates, and a potentially continuing contraction in the manufacturing sector.

Government Measures and Bank of Thailand's Stance

Despite these challenges, the Thai government has a budget and fiscal measures aimed at stimulating investment and increasing domestic consumption without significantly increasing government debt. Infrastructure projects are accelerating, improving connectivity, efficiency, and job opportunities.

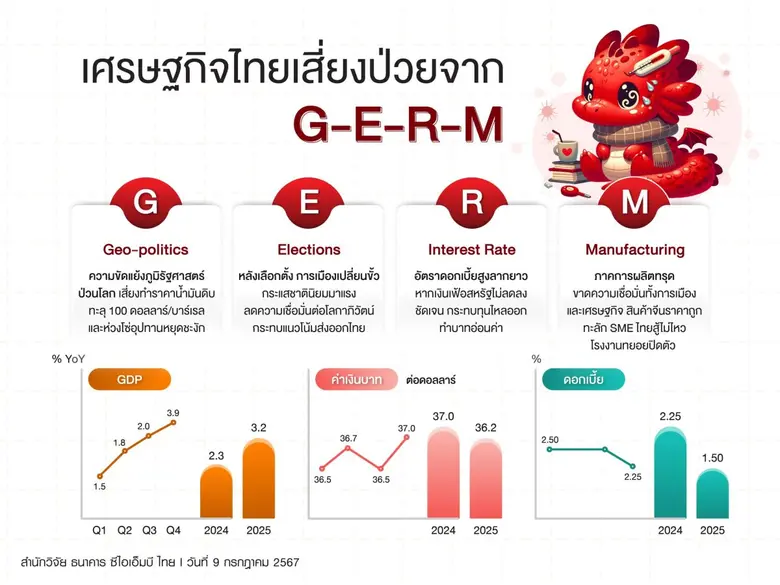

The Bank of Thailand (BoT) maintained its policy interest rate at 2.50% in the June 12 meeting to keep household borrowing in check due to concerns about long-term financial stability from rising household debt. The BoT also promotes responsible debt management among households and considers debt restructuring programs for those facing financial difficulties. Inflation remains within controllable limits, and the economic recovery aligns with the BoT's expectations, indicating no urgent need to cut interest rates to spur growth. However, a 0.25% rate cut to 2.25% is expected in the December meeting to stimulate economic growth in 2025 and align with declining Thailand's potential growth rate.

We forecast the Thai Baht to appreciate from 36.7 THB/USD at the end of June to 36.5 THB/USD by the end of September, expecting a U.S. rate cut in September, easing market liquidity concerns and attracting capital flows into emerging Asian markets. However, by the end of 2024, we expect the Baht to depreciate to 37.00 THB/USD due to rising uncertainties in the U.S. economy, particularly regarding the U.S.-China trade war during the U.S. presidential election period.

Key Growth Drivers:

- Tourism: Tourism is a key growth driver, with expected tourist numbers reaching 35.6 million in 2024 and 39.1 million in 2025. This recovery is likely to boost services like hotels, restaurants, transport, and retail, improving employment and wages in the mid-to-high-end market. However, the budget tourism sector, reliant on Chinese tour groups, may not fully recover as Chinese tourists currently returned about 60% of pre-COVID levels.

- Household Consumption: Expected to be supported by increased consumer confidence and household spending, backed by government stimulus measures such as utility subsidies and cash handouts to targeted groups. The plan to distribute 10,000 THB digital wallets could further boost economic growth by 0.2%, raising the 2024 growth rate from 2.3% to 2.5% if implemented this year. Overall consumption may still face challenges due to decreased purchases of vehicles and durable goods, though services are expected to continue expanding well.

- Investment: Private investment is anticipated to grow with the recovery of the export manufacturing sector. Public investment is also expected to expand following the budget allocation, particularly in infrastructure development. Accelerating public investment is crucial for boosting investor confidence, especially in attracting foreign direct investment (FDI) to the Eastern Economic Corridor (EEC), which is expected to show clearer progress in Q3.

- Exports: Exports are expected to recover well, supported by global trade recovery and demand for Thai products. The US-China conflict may benefit Thailand through increased trade with the US, supporting the manufacturing and employment sectors, especially in electronics and processed foods.

Economic Risk Factors for Q3 - GERM:

- Geo-politics (G): Investor confidence may decline, shipping costs could rise, and oil prices may spike, particularly affecting production and transportation costs. The Brent crude oil price, forecasted at $82 per barrel, could exceed $100 if geopolitical tensions worsen, especially involving major oil producers like Saudi Arabia, Iran, or in the Ukraine conflict, impacting Russian oil supplies. Conflicts between China-Taiwan or North-South Korea could disrupt supply chains, increasing prices, especially in electronics.

- Elections (E): Elections in multiple countries can shift political power, affecting confidence in reducing public debt and impacting currency and economic growth. Notably, the US presidential election on November 5th is crucial for trade, investment, and de-globalization trends, potentially affecting the Thai economy.

- Interest Rates (R): While the Fed may cut interest rates in September and December, keeping them at high levels throughout the year could raise US government bond yields, reducing the appeal of risky assets in emerging markets. This could lead to capital outflows from Thailand, weakening the baht beyond the forecasted 37.0 to possibly 37.5 baht per USD, impacting import costs, especially oil, and increasing inflation, potentially causing the Bank of Thailand to maintain high interest rates.

- Manufacturing (M): The manufacturing sector's weakness has hindered Thailand's economic performance, including a lack of in-demand technology products, limited FDI growth, and competition from cheap Chinese imports. Continuous MPI decline is concerning, even though Q3 is expected to improve. However, if China continues to offload excess production in ASEAN, especially Thailand, it could force SMEs to shut down, affecting employment and consumption. The Thai government needs clear strategies to address Chinese product inflows and support SME adaptation.